In America, news reports abound regarding the recent FCC auction of AWS spectrum which resulted in over $44B in license fees bid. Farther afield in Sub-Saharan Africa, similar events are occurring but with much lower visibility. Recently, MAAS Telecom assisted the Ministry of Posts and Telecommunications of the Republic of Cameroon in the renegotiation of the existing MTN and Orange mobile licenses. Unlike in the US and Europe, spectrum in Africa is typically granted for a fixed period of time, usually between 10-20 years. In Cameroon, both Orange (aka, France Telecom) and MTN (based out of South Africa) received their initial license in the year 2000, both with a duration of 15 years. In 2014, the process to renew the mobile concessions was started and MAAS Telecom was asked to assist MPT in determining the value of the renewal fee and the major business terms of the license concession.

To determine the value of the license, we developed a “bottoms up” model that projected the future financial results of the respective businesses. Since both Orange and MTN are public companies, we were able to utilize their publicly available information as a starting point. In 2013, MTN Cameroon reported approximately $529M in revenue and $250M in EBITDA. Orange Cameroon reported approximately $373M in revenue and $140M in EBITDA. Both had also reported interim results for 2014. Our model utilized expected future mobile penetration, GDP growth, GDP/capita, and expected ARPUs to project out financial results for the future 10-15 years. We also factored in the impact of a third mobile operator and the existing incumbent player, CAMTEL, into the projections. With only 65% mobile penetration, significant duplicative SIMs, and single-digit Internet use, the prospects for the continued growth of the Cameroon telecom/Internet market are strong.

For business terms, mobile operators in Africa facing renewals are focused on a few high level terms: adequate spectrum, technology neutral licenses, restrictions on outsourcing and of course, price. After significant negotiations, which even extended past the actual expiration of the current mobile licenses, both MTN and Orange signed new mobile concessions last week which included 3G/4G capability and a 15 year term. MTN and Orange agreed to each pay FcFA 75 Billion, or approximately $150M USD for the mobile concession.

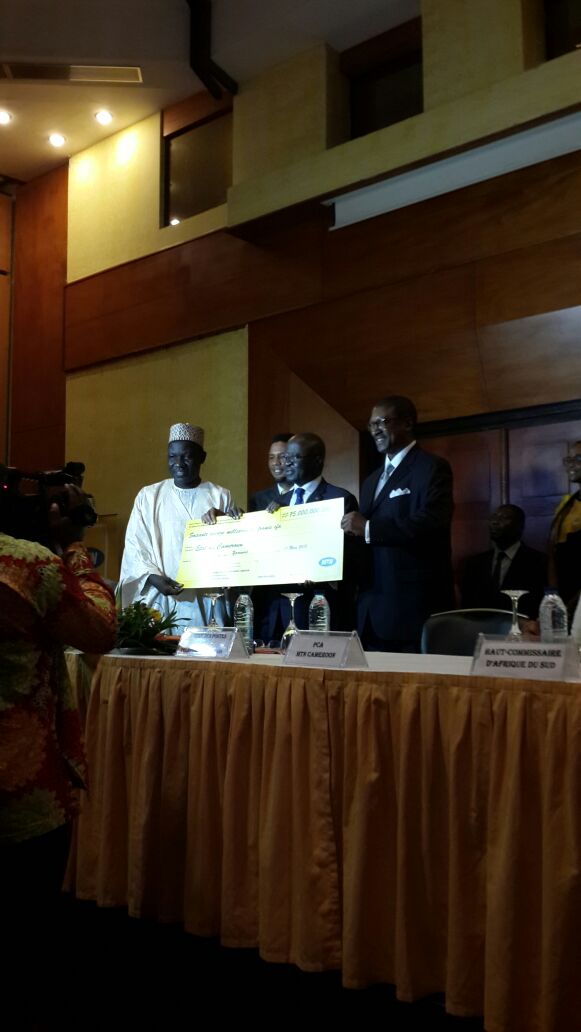

The picture to the right shows the signing ceremony with MTN and top Cameroon government officials. The completion of this project portends good things for the continued development of the Cameroon mobile market with three sophisticated, deep pocketed operators competing to bring mass-market Internet and voice services to all Cameroonians. MTN Cameroon has already launched 3G service, meaning they had already upgraded their 2G network in expectation of a favorable renewal.

88MPH Incubator in Nairobi, Kenya

In September I visited Kenya to meet with some local telecom and Internet companies. One of the firms I met was Kili.io. Kili is a managed hosting business run by Adam Nelson. Adam recently relocated from NYC where is was active in the tech scene working at a number of Internet businesses, most recently as the CTO of Yipit. I met Adam at his office location, an incubator called 88MPH. The office is in a busy commercial district in Nairobi. Getting off the elevator and stepping into the office, one would be forgiven for thinking they are in NYC or San Francisco. The open layout, groups of young programmers hacking away at desks and overall environment of activity and excitement permeates the space. I was instantly intrigued.

Kili.io is bringing public cloud infrastructure to African markets. They are in the pilot phase currently in Kenya with a focus on supporting SMEs and startups and have a target launch date of January 2014. As some readers might know, Nairobi is the hub for sub-Saharan African startups and so it is the natural place for many new companies to prove their products before rolling them out to the other markets in the larger region. The region has coined a new phrase for itself- the “Digital Savanna”.

Because cloud infrastructure is deployed around the world by various vendors using proprietary technologies, Kili has taken a standards based approach around OpenStack – a set of standards agreed to by IBM, HP, Cisco, Rackspace and others so as to keep clients comfortable that there is no vendor lock-in or proprietary technology that keeps them tied down. The APIs used by Kili are also Amazon Web Services-compatible so that savvy organizations can take advantage of multiple clouds based on their regulatory and performance needs. The pricing model is “pay-by-the-drink”, similar to AWS, and the company offers compute, connectivity and storage options for small and large workloads. The company hopes by mid-2014 to expand to other regions outside of Kenya including South Africa and Nigeria – where much of the demand lies for infrastructure services.

While cloud is relatively new to African consumers, the business logic for local infrastructure is compelling. Because of a lack of quality hosting companies like Kili, most content is still hosted in Europe or the United States. This means that when a Kenyan eyeball hits the local Kenyan newspaper’s website, the packets travel out the country, over submarine cables to Europe, through terrestrial fiber to Amsterdam onto a server to retrieve the page and back again. Ridiculous. Kili which is hosted in a Tier III datacenter location near the Kenyan Internet Exchange will be able to dramatically improve performance for web properties. The user experience will improve tremendously, and this should propel demand and the development of additional content. And the teams intimate knowledge of Internet Infrastructure and application management means that customers will be confident to entrust their hosting needs to Kili.

Given my former tenure at Voxel dot Net and familiarity with the hosting space, I was immediately impressed with Adam and his team and the problem they are trying to solve. As I’ve stated in other blog posts, my view is that the Internet in Africa is poised for strong growth and managed hosting will be a necessary component of its development. After my visit Adam and I continued our conversations, decided to partner together, and today I am an investor in the business. We are excited about the prospect of bringing world-class hosting capabilities to the African market.

I attend the Capacity Telecom Africa conference in Dar es Salaam, Tanzania two weeks ago. It was my third time attending a Capacity Africa conference and like previous ones I found the event informative and interesting. It continues to be well attended with most major African, European and Asia carriers present. This year I noticed more American firms, most prominently Verizon and Level 3. The major themes in Africa telecoms from the last few years are continuing– mobile subscriber growth, termination of submarine cables and build out of national and metro fiber networks. Obviously, Africa is a huge continent with 50+ sovereign nations so these types of projects will take longer than the trajectory that occurred in large countries like the US, China or Brazil. But there was definitely a new element at the show that has not been as prominent in past events: the emergence of Internet Infrastructure in Africa. One of the big announcements at the show was that the Amsterdam Internet Exchange, one of the largest Internet peering points in the world, had partnered with Seacom, a East Africa submarine cable company, to extend the AMS-IX into Sub-Saharan Africa. The idea will be to provide “virtual ports” to African Internet players so that they can begin to interconnect with networks on the AMS-IX peering fabric. In addition, the AMX-IX East Africa will enhance connectivity with the East Africa region by providing a local interconnection point for African Internet traffic. Internet traffic in Africa many times “hair-pins” through London, US or Amsterdam (so called, “scenic routing”) so keeping traffic local will enhance performance and dramatically lower costs.

I attend the Capacity Telecom Africa conference in Dar es Salaam, Tanzania two weeks ago. It was my third time attending a Capacity Africa conference and like previous ones I found the event informative and interesting. It continues to be well attended with most major African, European and Asia carriers present. This year I noticed more American firms, most prominently Verizon and Level 3. The major themes in Africa telecoms from the last few years are continuing– mobile subscriber growth, termination of submarine cables and build out of national and metro fiber networks. Obviously, Africa is a huge continent with 50+ sovereign nations so these types of projects will take longer than the trajectory that occurred in large countries like the US, China or Brazil. But there was definitely a new element at the show that has not been as prominent in past events: the emergence of Internet Infrastructure in Africa. One of the big announcements at the show was that the Amsterdam Internet Exchange, one of the largest Internet peering points in the world, had partnered with Seacom, a East Africa submarine cable company, to extend the AMS-IX into Sub-Saharan Africa. The idea will be to provide “virtual ports” to African Internet players so that they can begin to interconnect with networks on the AMS-IX peering fabric. In addition, the AMX-IX East Africa will enhance connectivity with the East Africa region by providing a local interconnection point for African Internet traffic. Internet traffic in Africa many times “hair-pins” through London, US or Amsterdam (so called, “scenic routing”) so keeping traffic local will enhance performance and dramatically lower costs.

Another example was the announcement by Liquid Telecom of the establishment of the East Africa Data Centre company. Liquid Telecom, which is based in London, is one of the largest independent fiber networks in Sub-Saharan Africa with over 13,000km of fiber infrastructure across Kenya, Uganda, Rwanda, Zambia, Zimbabwe, Botswana, DRC, Lesotho and South Africa. Liquid acquired the EADC via its acquisition of Kenya Fiber Networks, a Kenyan based fiber company in February of this year and has decided to spin out the datacenter business into a separate company. I met some of the Liquid folks at the event and they were kind enough to invite me to visit the facility in Nairobi. Nairobi is less than two hours from Dar es Salaam and served by daily departures so I hopped a plane on Wed to visit the facility. The EADC is an impressive building with over 20,000 sq.ft. of technical space. The building is surrounded by a high wall and secured via external guard house and security desk at the main building. The first floor of the facility has been fitted out and sold to customers and they are now building out the second floor. The floor is served via N+1 UPS feeds with about 1.2MW of power and backed up by onsite battery and diesel generators. I asked the Datacenter Manager who gave me the tour if they regularly tested the back-up systems. He looked at me with a quizzed look on his face and said, “Of course, every day”. The power grid in Africa frequently fails so reliable, redundant back-up facilities are a must. The building is served by over 5 fiber providers with physically redundant entrance facilities. All in all, an impressive operations and one that should allow for the continued expansion of Internet businesses in Kenya and East Africa.

It is clear to me that the next phase in the evolution of the telecom sector in Africa is here with the focus on building a robust and pervasive Internet ecosystem like has occurred in other continents.

Appcore Converged Infrastructure

I recently joined the board of directors of a company called Appcore (www.appcore.com). I was introduced to the company via the investment banker managing the raise of their Series B round. I was instantly intrigued by their story since the company’s converged infrastructure platform targeted telecom service providers and data center operators. This focus struck a cord because when I joined Voxel dot Net, a managed hosting company in January 2011, one of our initial sales targets were telcos, many of whom I knew personally from my 15 years in the telecom space. The sales premise went that telecom players wanted to sell cloud and managed services to their customers but lacked the in-house expertise to build and manage public/private clouds so partnering with an IaaS player like Voxel through a wholesale relationship was a natural fit.

We probably had a dozen very positive initial discussions with telcos, MSPs and collocation providers about the Voxel platform. Based on the initial discussions, I expected many to evolve into commercial relationships. But as we delved deeper into the details an unfortunate reality became clear. The truth was that that highly automated cloud platforms like Voxel’s VoxStructure (and for that matter others like AWS, RackSpace and Softlayer) were simply too complex for telcos to manage. Voxel’s automated infrastructure was more of a “toolkit” that telcos would have to utilize to build actual products and services for their customers. In addition, the process of configuring, provisioning and managing clusters and specific applications ultimately had to be handled by the telcos for a wholesale relationship to work. Telco’s simply did not have the depth of knowledge in systems administration and application management across the organization to manage an IaaS platform via a wholesale model. We sadly discovered this fact after a few months of discussions and ultimately terminated our sales activities to this sector.

What I’ve discovered since joining Appcore is that most telcos are in the same state as they were in 2011 – still trying to get their heads around how to deploy cloud and applications to their customers. Most telcos have still not made the paradigm shift from networking to cloud/managed services absent those that have completed major acquisitions, such as CentryLink’s acquisition of Savvis and Verizon of Terremark. This is why I am so excited about the Appcore solution. The Appcore platform is designed to enable service providers to offer cloud services and applications to their customers. The Appcore platform is designed from the ground up to be a service provider owned and operated infrastructure stack with end user products and services (geared toward SME and enterprise customers) pre-built into the system via an enterprise app store and easy to use provisioning and orchestration front-end. Appcore’s solution allows our telecom service providers and datacenter customers to be selling a fully branded public/private cloud product set on infrastructure that they own to their end user customers in 45 days.

The flagship Appcore product is called Appcore AMP for “Automation Management Platform”. The AMP product automates the deployment, management and orchestration of compute, storage and applications for enterprise private clouds and service provider public clouds. The AMP software stack is technology agnostic (hardware, hypervisor, storage type, etc), allows for granular management at the VM level and includes bare metal and virtualized server integration all through a single interface to multiple clouds and zones. From a deployment perspective, the Appcore solution is delivered in three modes: as a fully integrated hardware/software bundle that we ship in half rack or full rack deployments; as a 2U software appliance that manages customer owned equipment; or as a fully outsourced white label solution. As we like to say, we can deploy AMP on “your hardware, our hardware or no hardware.” The multi-zone orchestration capabilities of AMP mean that hybrid deployments are seamless. In fact we have multiple customers who have an Appcore deployment with Zone 1 on their premise and Zone 2 at our datacenter facility in the MidWest US. Under the hood, AMP leverages Cloudstack, Openstack and Puppet with a large amount of proprietary code and intelligence.

Already, several of the telcos that I spoke to about cloud services in 2011 have become Appcore customers. The attraction of the Appcore solution is not just the elegant technical capabilities of the system, but the completeness of the Appcore solution. Appcore has really thought through how to enable service providers to be successful at selling cloud to their end-user customers. This is why the Appcore tagline is, “Appcore – the business of cloud computing.” Appcore has developed an extensive video training library for operations, sales and marketing, created generic marketing and product collateral, and provides extensive onsite training. Why? Simple, the better Appcore customers get at selling cloud, the more infrastructure they will consume, and the more money both parties make. Appcore has a strong incentive to make their customers successful, unlike other products that are focused on onetime license or hardware sales. I’m excited to be working with Appcore and strongly believe that this type of approach will allow telecom service providers, MSPs and data center operators to enter the business of cloud computing.

Sponsors of the 2013 Summer Hosting Event

On June 12th, MAAS Telecom and several other NYC-based firms in the hosting and cloud infrastructure space sponsored a networking event for the community of hosting providers, cloud service vendors, telecom operators, datacenter managers and investment parties involved in the ever-growing infrastructure service industry. The turnout was fantastic and a large swath of the infrastructure market was represented to network, discuss recent trends and learn about product success and adoptions.

The event included a special presentation by Phil Shih of Structure Research, in which he gave an overview of the hosting sector and an analysis on recent events, including Rackspaces earnings report and the acquisition of Softlayer by IBM. Phil has offered MAAS Telecom partners a free copy of his report. Please contact us for an introduction.

The attendees included leaders and representatives the following firms:

|

|

The industry continues to grow and mature, even as more complex growth stories are emerging. We continue to stay actively involved with providers across the industry to keep track of this fast moving market.

Accra, Ghana

I just returned from my first trip to Accra, Ghana where I was able to meet industry officials, several operators and a few broadband/Internet players. Economically, Ghana is booming with 8% growth projected this year. The country is benefiting from recent discoveries of oil and natural gas, as well as continued strong demand for gold. Formerly know as the “Gold Coast” during colonial times, Ghana is the second largest exporter of gold after South Africa on the continent. However, it was obvious from my visit that the economic story is much broader than just commodities. Real estate is booming with new office buildings and residential units going up everywhere. One development my guide informed me would be home to Ghana’s first Ferrari dealership. I was also impressed by the number and variety of service and retail businesses. In driving around Accra to meetings, I saw many financial services, medical, banking and niche consumer businesses, much more than in other African countries that I have visited. In general, buildings and roads are well maintained and modern. (more…)

Viettel Grouo

In my travels around Africa I have come to meet the Viettel Group. Viettel is the dominant mobile phone company in Vietnam. Starting in 2004, it has grown to be the largest mobile operator in the country with over 55M customers. Since 2006, they have been expanding internationally, first to neighboring Laos and Cambodia and most recently to Haiti, Mozambique and Peru. They are currently the 19th largest mobile provider by subscribers and recorded over $6B of revenue and $1B of net income in 2011. (more…)

![]() I recently attended the Capacity Africa Telcom Conference in Dar es Salaam, Tanzania. This was the second time I had gone to the Africa conference, the last one being in Nairobi, Kenya in September 2010. The Africa telecom scene is one of the most dynamic and rapidly growing in the world. While aggregate revenues in the telecom space in the US, Europe and Japan are stagnant to down, growth in African telecom clips 10-25% per year. The core focus over the last 5-7 years has been in the adoption of mobile phones. In 2005 there were 133M mobile subscriptions on the African continent, in 2011 over 500M. (more…)

I recently attended the Capacity Africa Telcom Conference in Dar es Salaam, Tanzania. This was the second time I had gone to the Africa conference, the last one being in Nairobi, Kenya in September 2010. The Africa telecom scene is one of the most dynamic and rapidly growing in the world. While aggregate revenues in the telecom space in the US, Europe and Japan are stagnant to down, growth in African telecom clips 10-25% per year. The core focus over the last 5-7 years has been in the adoption of mobile phones. In 2005 there were 133M mobile subscriptions on the African continent, in 2011 over 500M. (more…)

Role: Investor, CEO and Board Member

———-

Activities: Joined company as CEO in January 2011 and led $5.5M Preferred Equity & Debt financing in March 2011. Consumated sale to Internap Network Services Corp., (NASDAQ: INAP) in January 2012 for $35M in cash.

Role:Senior Advisor

———-

Activities: Served as a Senior Advisor to $4.5 billion hedge fund, advising on investment opportunities in the telecommunications and media sector. Monitored portfolio companies on strategic and tactical initiatives, originated investment ideas and consulted Credit Committe and Chief Investment Officer on investment opportunities.